‘Using life insurance as an alternative to holding assets in trust’ by Jacob Fay published in IFA Magazine

Within estate planning, the debate between procuring life insurance versus placing assets into trust is one that often arises. Both avenues offer distinct advantages and serve unique purposes, yet the choice between them hinges on individual circumstances, financial goals, and the specific needs of the beneficiaries.

Where you have trust funds for younger lives you might want to consider both the impacts of the 10 yearly periodic charges and the annual accounting costs. When opting for a trust, the periodic charges and administrative overheads can accrue over time, potentially impacting the overall value of the assets held within the trust. Moreover, the meticulous record-keeping and reporting obligations can add to the administrative burden, necessitating ongoing attention and resources. It can be useful to compare this to the costs of maintaining a life insurance policy.

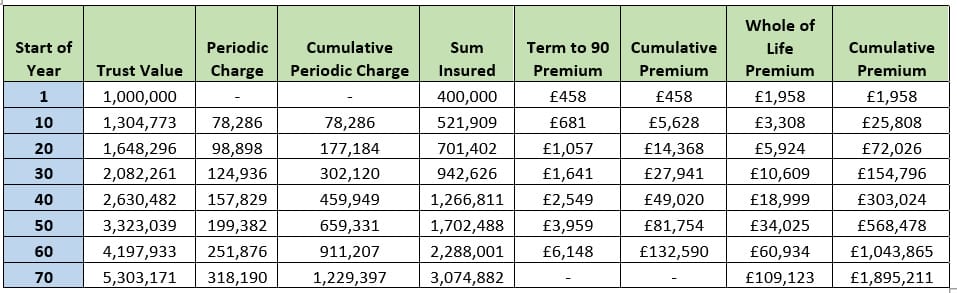

The below illustration is based on an initial trust value of £1m and an equivalent sum insured with IHT at 40% if the assets were not held in trust. We have assumed a fund growth rate of 3% annually and an equivalent 3% escalation of the sum insured, with premiums increasing by 4.5%. The client is a 26-year-old non-smoker.

When comparing the cumulative periodic charges with the cumulative premiums over both the short and long term, for a term life insurance policy running until age 90, the total cost of purchasing life insurance is significantly cheaper. Even when comparing the cost of purchasing a whole of life policy, the premiums would only surpass the cumulative periodic charges when the client reached age 79. Additionally, this comparison does not factor in any costs associated with the trust except the periodic charges. As such, the overall trust charges may be higher meaning the costs of whole of life cover would remain the cheaper option.

Taking out a life insurance policy to cover the IHT liability on the assets can provide a simple and cost-effective solution in comparison to placing assets into trust. Paying an annual premium of either £458 or £1,958, in this instance, is far more manageable and the planning is less complicated than co-ordinating the cash necessary for payment of a 6% periodic charge.

One important point to consider is that the trustees may not wish to release assets to younger beneficiaries. A primary concern for trustees can be the beneficiaries’ maturity and financial responsibility. Younger individuals may lack the experience and judgment needed to handle significant sums of money wisely. Handing over a substantial inheritance too soon could disincentivise them from pursuing their own ambitions and achieving financial independence through their efforts.

Secondly, depending on the assets within the trust, there may not be sufficient liquidity to pay the periodic charges. Illiquid assets, such as property, art portfolios, or other types of investments, may not generate regular income or easily convert into cash. As a result, trustees may face difficulty in raising the necessary funds to cover the ongoing and periodic charges.

Unlike liquid assets, which can be readily sold or converted, illiquid assets may require time-consuming processes to generate cash. Trustees might need to sell the assets in the market, find suitable buyers, or navigate complex valuation procedures, leading to delays in accessing funds for periodic charges.

The illiquidity of certain assets can create cash flow issues for trusts, requiring careful financial planning and strategic decision-making by trustees to ensure that the trust remains adequately funded and can fulfil its financial obligations over time. A life insurance policy can provide an easy to administrate and low-cost alternative to holding assets in trust.

Author: Jacob Fay, Protection specialist at John Lamb Hill Oldridge

Article published in IFA Magazine in January 2024.

Other Insights

Jacob Fay shortlisted in the UHNW Services Individual of the Year category at the Citywealth Future Leaders Awards 2026

We are delighted to share that Jacob Fay, Associate at John Lamb Hill Oldridge, has been shortlisted in the UHNW Services Individual of the Year category at the Citywealth Future Leaders Awards 2026. The Citywealth [...]

Ken Maxwell shares his insights on why younger generations remain under-protected and why the conversation needs to change in IFA magazine

Ken Maxwell, Director at John Lamb Hill Oldridge, has been featured in two recent IFA Magazine publications exploring why younger generations remain under-protected and how advisers can help change the conversation. Alongside contributing to an [...]

Video interview: “Whole-of-life is only to ‘protect the assets you’ll die living in and living off’” published by FT Adviser

Holly Hill, Director at John Lamb Hill Oldridge, recently spoke with Sonia Rach at the FT Adviser about the role of life insurance in inheritance tax planning for high-net-worth and ultra-high-net-worth clients. In the interview, [...]